Buying a home is the American dream, but sometimes there are hurdles making ownership a struggle to many. Down payment, higher debt ratios, and credit requirements make buying a home difficult at times. Many are familiar with the benefits of an FHA, VA, or USDA loan in these cases. But there is a conventional loan providing a great option and it is not just for first time buyers. This loan is called the Fannie Mae HomeReady mortgage. The HomeReady loan gives buyers several benefits and some are unique to this product. So when buying a home with a lower down payment, consider these benefits of the HomeReady mortgage mentioned here.

HomeReady Benefits

- Lower Payments

- Low Down Payment

- Flexible Credit Guidelines

- Not Just First Time Buyers

HomeReady mortgage loans are created to compete with the FHA loan. Just like FHA loans, HomeReady mortgage lenders provide affordable financing to today’s buyers. There are so many features that combine to create these 5 benefits above.

HomeReady Low PMI

In order to lower home loan payments, HomeReady allows for a lower than normal mortgage insurance. Mortgage insurance (PMI) allows lenders to lend a higher percentage of the purchase price. Because this Fannie Mae loan has lower PMI, the total house payment is lower! Since there is mortgage insurance on these loans, the down payment requirement is as little as 3% of the purchase price. Plus this down payment may be a gift or allowed grant.

HomeReady is Flexible

So HomeReady has lower payments and low down payments. But there are some other features that aren’t as prominent. Typically conventional loans reward higher credit score borrowers, but this Fannie Mae loan is more flexible. With the lower mortgage insurance percentage, it even helps borrowers with not so perfect scores. Furthermore some buyers need help with a higher debt to income ratio. Often buyer debt ratios are higher because of student loans, but this program may help achieve ownership.

High Debt Ratios

Solutions for higher debt ratios include boarder income. Boarder income is rent received from a roommate. Although it is only allowed when there is a documentable history of receipt.

Finally, this wonderful program is for first time buyers, relocators, retirees, move up buyers, and even down sizing buyers. When you find the perfect home on Zillow, Trulia, or Homes, check with us for the right mortgage. Our team of experts will see if HomeReady works for you.

How Does HomeReady Mortgage Insurance Help Me?

As mentioned earlier, HomeReady mortgage loans offer lower mortgage insurance. Typically a 3% down payment mortgage requires a higher rate of PMI. Technically it is a 25% coverage compared to the more normal 35% coverage. All you really need to know is that means lower PMI or lower payments. Foremost, a mortgage payment is made up of principal and interest, which pays back the money. Next you have the escrows for taxes and insurance. Then in most cases where less than 20% is put down, there is mortgage insurance. Since PMI is one of the 5 parts of a mortgage payment, you want it to be as low as possible. Additionally, once the loan balance has been paid down, it could be cancelled. Don’t forget that PMI on a primary residence may be a tax deduction for many buyers. So consult your tax advisor.

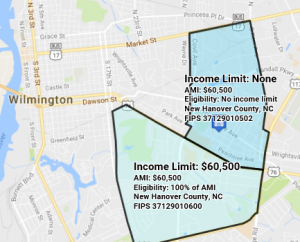

HomeReady Income Limits

Like some of the other affordable housing loans, there are maximum income limits for borrowers. Unlike USDA which uses a household income limit, HomeReady Income Limits only use the borrower’s income. If this loan type is a possibility, lenders will check the HomeReady income limits page. Although there is an exception to exceed the income limits! Most counties have areas where the income limits do not have to be met. So always look up the location of the property as the property may qualify for the exception. Check out one of the areas in Wilmington NC which does not require an income limit. So a buyer making $100,000 per year could purchase with only 3% down payment!

HomeReady Vs FHA

As we already mentioned, Homeready offers a reduced mortgage insurance premium compared to a normal Fannie Mae loan. So how does it compare to FHA and which one should I choose? First of all, both loans are excellent choices for buyers. But sometimes there are reasons to choose one over the other. No one loan is best for every situation.

Low Credit Scores Favor FHA over HomeReady Loans

Low credit scores typically match up better with FHA loans. As credit scores get down into the 600’s, then FHA wins the battle. Plus the lower the score, the more chances of the right choice being FHA. Why is that? Since FHA is a government loan, the rates do not fluctuate as much with lower credit scores. For instance a 640 credit score may be practically the same rate as a 760 credit score buyer. Plus no matter the credit score, FHA mortgage insurance is the same. So a 600 credit score buyer with a 30 year fixed rate loan would have the exact same mortgage insurance as an 800 score buyer. This is definitely not the case with a conventional loan like HomeReady.

High Credit Scores May Favor HomeReady Mortgages over FHA

Alternatively, conventional loans really favor buyers with higher credit scores. One of the benefits with this conventional loan is not having the up front FHA mortgage insurance. This saves 1.75% of the loan in costs up front no matter what the credit score is. Furthermore because of the low mortgage insurance offered by HomeReady, it is often a lower payment than FHA. Then there is the fact that PMI could be cancelled once under 80% of the original price on a conventional loan. If living in the house a long time, this could be another factor to consider in comparison to FHA. FHA requires lifetime PMI when the buyer puts down less than 10% down payment. Either way, I will compare the options that make sense for buyers.