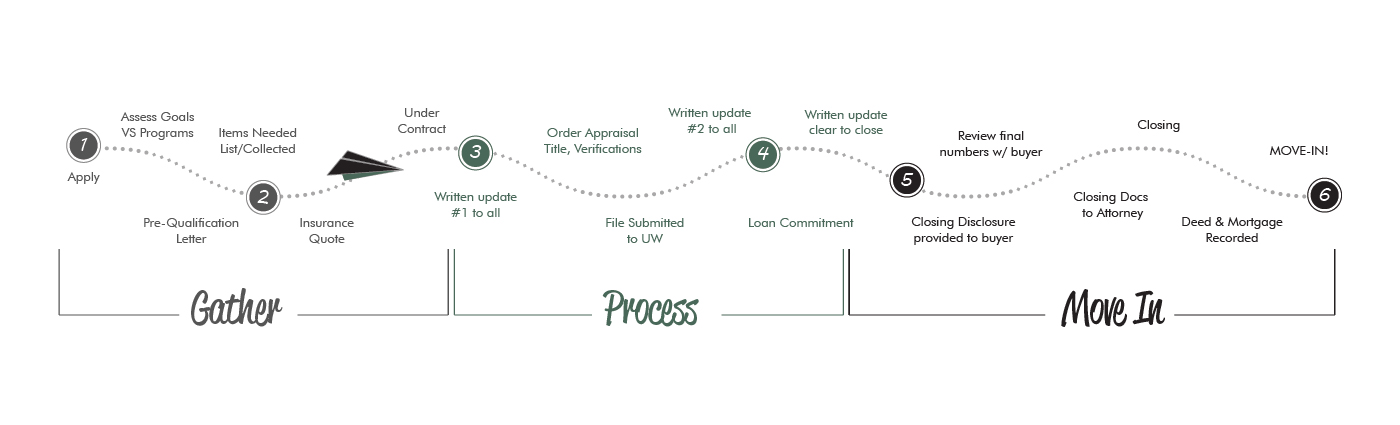

Some of these circumstances you may think are obvious and others just don’t seem right. But they can kill your mortgage loan potentially at the very last hour. When buying a home, the best advice we can tell you is to be very boring and “Steady Eddie”. This includes before and during the mortgage loan process. In a perfect scenario, lenders love to see long tenures on the same job and with the same employer. Other positives include credit length, not moving money around, and no credit inquiries. Some of these items may not deny a loan but it could at least cause delays or more paperwork at a minimum.

Mortgage Loan Process – Top 10 “What Not To Do When Buying a Home” Tips:

While in the mortgage loan process, avoid these examples to make your closing easier.

- Teacher quit job in June for a purchase closing in July. Borrower’s response: “I’m a teacher and we take off the summer anyway so I will find another job somewhere when school starts back”. We couldn’t believe this answer but this did not work and had to wait until the borrower got a new job. Unless your mortgage lender is definitely using other income like retirement or social security only, DO NOT quit your job! Lenders will find out when a final verbal verification of employment is performed. This is not the time to find out.

- Borrower changed jobs in the mortgage loan process from an hourly nursing position of many years to a position as a traveling nurse being paid as PRN. Most of the income came from mileage reimbursement and a smaller hourly pay. The borrower saw it as making more money because much of the new income was nontaxable but lenders will not count this new income as it didn’t have a history plus it is really just reimbursement and not consistent amounts. Be very careful when considering a job change as it could be better in ways but may not work for your home purchase, at least for a while.

- Borrower paid off medical collections without having them deleted. It took a while for the borrower to find a house so a new credit report was pulled when a property was chosen and the prior credit expired. The credit scores dropped 100 points! The reason for the drop: If a collection that has a date of last activity of a few years ago is paid off now, the date of last activity changes to NOW. It is like new collection activity and the credit score can drop significantly. This makes no sense and most of the general public doesn’t know this. But this is what happens currently with credit scoring systems. There is talk of this changing in the future so paying off a collection won’t hurt a credit score. So do not pay off collections in the mortgage loan process.

- Changing from hourly / salary income to commissioned. Do not change from hourly or salaried income to commissions during or just before the mortgage loan process. At minimum, borrowers must have a 1 year history of commissions reporting on tax returns to figure an average. But often it can even be 2 years of history before including the income on a mortgage. For example, if someone changes from $4,000 monthly salary to $2,000 base and commissions of approximately $2000 per month, $2000 per month will be used as income and not $4000!

- Changing jobs from w2 to 1099 income. Be careful. We had one couple that were doing everything right before going under contract on a house. They even asked if the wife changed jobs with the same position, would be ok. So we talked at length about making sure that the new job is salaried, w2’d, etc. We gave the ok as long as the new job could be verified as discussed. Wouldn’t you know, the borrower started the new job and found out that new job was actually paid as a contractor. The position was 1099’d even though the interview said it was w2! So the borrower became brand new self-employed . This means zero income could be counted in this case since there is no history on the most recent tax returns. The employer didn’t think anything of it but obviously this made a big loan issue to the borrower’s home purchase. Luckily this ended as a happy ending because the borrower qualified on his income alone. The co-borrower was happy with her new job and the purchase closed.

- Don’t stop paying your bills on-time during the mortgage process! We couldn’t believe it when we re-pulled a final soft pull credit report 2 days prior to closing – 4 credit card accounts were all 30 days late just before closing! The answer we received when brought up was “When we had to pay the $500 deposit on the purchase contract, we had to decide not to pay something so we could get the house”. So keep in mind, if you have to skip payments on bills to afford the earnest money deposit, it is not the right time for you to buy a house.

- Don’t go car shopping, it can wait! This happens the most of any of these No-No’s when the instant gratification of buying a new car steps in. Even if you are buying a new car that has a lower payment, make sure you talk to your mortgage lender first because one more credit inquiry could make your score go from a 640 to a 635. Then there is a potential turn down on a USDA loan for instance. Believe it or not, the borrower in # 1 above also got 2, yes 2, new car loans in the mortgage process. One was for the daughter and the answer was “but the daughter will make the payments”. That doesn’t matter!

- Don’t hide or forget to mention debts such as IRS or State Income Tax payment plans to your loan officer. These will be found out from the bank statements being reviewed later in the process. So make sure that you mention these type of things early in the process. An extra $300 in payments could cause a debt ratio to be too high for qualifying.

- Don’t co-sign on new accounts! Many think that co-signing on a new car or other type of loan will not factor in the borrower’s debt ratio. “I’m only a co-signor and the other person will be making the payments”. Always keep the following in mind: You are still on the hook just as much as the primary borrower. If the borrower is late or in default on the payments, it shows on your credit just the same. The debt will be counted in your debt ratio. If you have co-signed with someone and can provide the promissory note listing you as a co-signor, plus 12 month’s proof that the other person paid the creditor directly, it can often be excluded from your mortgage debt ratio.

- Don’t turn in your car! Some people think that letting a car go back voluntarily is ok, but whether you give it back or the company takes the car, it is reported as a repossession. Additionally, if the car is sold for lower than the balance, which it often is, you will owe a collection balance. This has happened a few times that we can recall over our 21 years in the mortgage business but many misunderstand turning a car in, so that is why this is mentioned.

We hope that this will save at least one purchase from being denied. No borrower or mortgage lender can error-proof a mortgage loan process. But hopefully these examples will help you remember to ask questions before you do something. We don’t mind answering questions. It is better to ask and it be no big deal, than not asking. Not asking could kill your home purchase. So remember, boring and Steady Eddie is better!

[av_button_big label=’Contact Team Move to Qualify For Your Mortgage Today’ description_pos=’below’ link=’manually,http://teammovemortgage.com/our-team/’ link_target=’_blank’ icon_select=’no’ icon=’ue800′ font=’entypo-fontello’ custom_font=’#ffffff’ color=’theme-color’ custom_bg=’#444444′ color_hover=’theme-color-subtle’ custom_bg_hover=’#444444′]

Let us help you Get From Here to Home!

[/av_button_big]

Follow our writer, Russell Smith, on ActiveRain. ActiveRain is a site that real estate professionals, buyers, and sellers may use to gain helpful knowledge.